Scope 3 Reporting Requirements

An Overview of New Reporting Requirements for Public Financial Companies

The SEC proposed emissions disclosure rules for Scope 3 emissions in March 2022.

Extensive comments and the expectation of lawsuits resulted in a final rule issued

in March 2024 that dropped the Scope 3 reporting requirements.

The SEC proposed emissions disclosure rules for Scope 3 emissions in March 2022.

Extensive comments and the expectation of lawsuits resulted in a final rule issued

in March 2024 that dropped the Scope 3 reporting requirements.

In the meantime, the state of California passed two bills in October 2023 that require Scope 3 emissions disclosures for financial firms doing business in that state. CA emissions reporting requirements are even more extensive than the SEC proposals. These emissions can easily account for more than 95 percent of total emissions for financial and other firms. This huge new reporting requirement opens the door to independent auditing and challenging of the reported results, so affected firms need to take this new rule seriously and to conscientiously conduct required analysis and reporting to avoid challenges to corporate CSR commitments. In short, financial firms will need to (1) report emissions of their residential mortgagors and CRE loan customers, (2) adhere to an accepted emissions accounting standard, (3) disclose their methodology and data sources to provide transparency regarding emissions associated with these customers, (4) use the "highest quality data available ... and improve the quality of the data over time.” Financial institutions outside California should also take notice as trends in California often lead to similar requirements in other states. This Web page summarizes the most relevant portions of reporting requirements for financial firms preparing to meet these requirements and summarizes calculation processes and available supporting data. New reporting requirements open the door to independent auditing and challenging of the reported results, so financial firms need to take this new rule seriously and to conscientiously conduct required analysis and reporting to avoid challenges to corporate CSR commitments. MAISY Scope 3 mortgage and CRE loan emissions products and services are the most advanced, accurate and cost-effective resources available to fulfill these new emissions reporting requirements. |

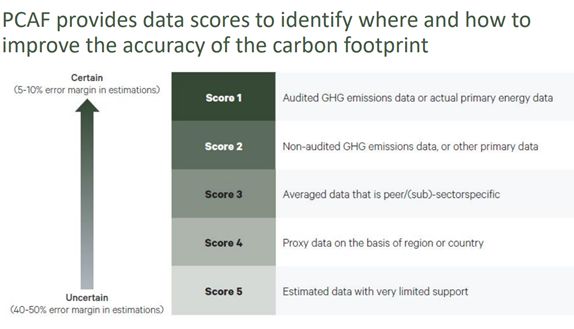

PCAF Standards Data OptionsThe Partnership for Carbon Accounting Financials’ Global GHG Accounting & Reporting Standard (the “PCAF Standard”) provides one methodology that complements the GHG Protocol and assists financial institutions in calculating their financed emissions. The PCAF Standard was developed for financial institutions to work with the calculation of Scope 3 emissions for the “investment” category of downstream emissions and was endorsed by the drafters of the GHG Protocol.Given the required nature of this reporting, financial firms will need to do the best they can in quantifying these emissions to protect against any claims of lax commitment to corporate social responsibility objectives. The PCAF standards are not particularly specific and in many instances are aspirational, so adopting this standard as a reporting methodology is relatively straight-forward. However, PCAF standards also states that “financial institutions shall use the highest quality data available for each asset class and improve the quality of the data over time.” The challenge using the PCAF standards is to achieve the greatest level of accuracy without imposing an “undue burden.” The PCAF standards are international so they attempt to rank lowest quality to highest quality data inputs with rather generic descriptions. This graphic from the 2019 PCAF North America Report suggests various quality levels.

US financial institutions will be evaluated on their emissions reporting based on available US data sources. At the top, the most accurate level would be for each mortgagor or CRE customer to report its emissions to the financial institution. This is obviously not realistic for US financial institution customers so the next best and most accurate option is to obtain actual energy use information for commercial customers where available or to estimate energy use information for residential and CRE customers based on statistical averages for geographic areas. Applying estimates with information on customer segment characteristics such as income and floor space will increase the accuracy of these estimates. For those looking to use publicly available data sources of estimated average energy use information for residential and commercial buildings energy use, there is no public source that provides information below the regional or sometimes state level, which as we document in the See the Notes and Whitepapers Section is critical for accurate carbon emissions reporting illustrating the advantage of MAISY ZIP-level energy use-based emissions data compared to state or regional averages. MAISY Scope 3 Emissions Data for Financial FirmsMAISY Scope 3 Databases are the most accurate available source of mortgage and commercial real estate loan financed emissions. Databases provide average electricity kWh, natural gas and fuel oil use for residential and commercial buildings in individual ZIP codes across the US. Segment averages based on residential income and floor space and commercial business type and floor space are recommended to enhance accuracy.For commercial real estate loan emissions, in addition to ZIP code business/floor space averages energy use information has been curated from CRE owners for more than 15,000 larger commercial properties in various US locations. MAISY Scope 3 Emissions Data for Financial Firms are developed from MAISY ZIP-level Utility Customer Energy Use Databases. MAISY Databases were introduced in 1995 and are updated on an annual basis. These data have been applied by some of the largest utilities, equipment manufacturers, state regulatory agencies, the US Department of Energy for appliance efficiency standards, and other energy related organizations to assess the same kind of utility customer data targeted by the new SCE proposed rules. |